Results of the latest IDC Asia/Pacific Semiannual Enterprise Applications Tracker show that the enterprise applications (EA) software market experienced good growth of 18.6% year-on-year (YoY) in the Asia/Pacific excluding Japan (APEJ) region in 1H 2011. IDC made this announcement today, Feb. 1.

Growth was mainly driven by the increased interest of companies to utilize enterprise applications for business process automation and faster time-to-value. But the upward trend in growth could be affected by the uncertainty surrounding the European economic crisis and the threat of a double-dip recession looming large in 2012.

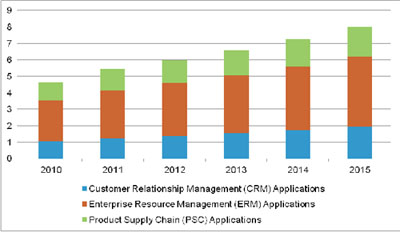

IDC expects these conditions to negatively affect the market and slow down growth and thus forecasts a compound annual growth rate (CAGR) of 10.2% to reach US$8.0 billion till 2015.

[ RMN Digital comments: In the fast-moving technology business where things change in a blink, it’s ridiculous to make long-term predictions, for say, 2015. Such researchers either don’t understand tech business or they deliberately try to hoodwink the buyers. You can choose to ignore such predictions. ]

“Although the need to extend newer functionalities and capabilities to end-users, which in turn help in improving internal efficiencies and reducing operating cost, has been driving growth over the last 18 months or so, companies will take a cautious approach on software investments in 2012 due to the negative economic scenario,” says Sabharinath Bala, research manager of IDC’s Asia/Pacific Enterprise Applications Software Research Group.

On the other hand, technology trends like cloud computing, mobility, analytics, social media, and the regulatory & compliance environment do not give organizations much of a choice, but to invest in new software or upgrade the existing software to accommodate these trends and remain competitive and compliant in the marketplace.

[ Also Read: Ali Shadman Reveals the Secrets of Cloud Computing ]

Hence vendors will have to focus on delivering the core value propositions for faster time-to-market, positive ROI, and business process improvement, rather than just concentrating on the factors like innovation, deployment flexibility, and platform integration, suggests IDC.

Key points from the IDC study include:

- Owing to critical demands of the business environment, most of the top tier vendors are adding vertical-specific applications to their portfolio, either through organic development – by incorporating industry-specific functionalities to their existing horizontals offerings – or inorganically by acquiring products from niche vendors.

- SaaS deployment of enterprise applications will gain traction, with small and medium enterprises opting for SaaS based offerings due to the low cost of deployment. This increased adoption of SaaS EA will cannibalize traditional on-premise deployments, but comparatively the overall size of the SaaS market will still be small.

- Vendor consolidation will continue, due to the eagerness of tier-1 vendors to acquire niche products and capabilities that will fortify their product portfolio. The drivers for vendor consolidation include technology trends like cloud, mobility, and socialytics.

At the secondary market level, enterprise resource management (ERM) market saw a minor increase in percentage share in 1H 2011 and stood at 52.1% as compared to 51.6% in 1H 2010, while there was a slight decline for product supply chain (PSC) applications; customer relationship management (CRM) market remained flat when compared between 1H 2010 and 1H 2011.

[ Also Read: Keep Your Friends Close and CIOs Closer ]

Although not the biggest contributor to the overall market, enterprise asset management (EAM) applications experienced the largest growth and manufacturing applications the least growth on a YoY basis among the functional markets.

In the picture above: IDC’s forecast on the APEJ EA market till 2015. The market is expected to grow at a CAGR of 10.2% and reach US$8.0 billion by 2015.

- Countries covered in IDC’s Asia/Pacific Semiannual Enterprise Applications Tracker include Australia, New Zealand, Korea, India, the PRC, Taiwan, Hong Kong, Singapore, Malaysia, and Thailand.

- Software revenue consists of license, maintenance, and other software revenue.

- Enterprise applications include enterprise resource management, customer relationship management, product supply chain management.